- What is Digital Certificate?

A Digital Signature

Certificate (DSC) is a secure digital key that certifies the identity of

the holder, issued by a Certifying Authority (CA). It typically

contains your identity (name, email, country, APNIC account name and

your public key). Digital Certificates use Public Key Infrastructure

meaning data that has been digitally signed or encrypted by a private

key can only be decrypted by its corresponding public key. A digital

certificate is an electronic "credit card" that establishes your

credentials when doing business or other transactions on the Web.

- Types of Digital Signature Certificates provided by eMudhra

Class 2 Certificates:

As

e-filing is made compulsory in ROC, every director / signing authority

needs to have their Digital Signature Certificate. Its now mandatory to

obtain Class-2 or Class-2 with PAN Encryption Digital Signature

Certificate for any person who is required to sign manual documents and

returns filed with ROC as per MCA21. Also an Individual is required to

obtain Class-2 DSC with PAN Encryption for e-filing his return with

Income Tax, India.

Class 3 Certificates:

2. Income Tax

3. Foreign Trade

4. e-tendering/e-procurement

5. Employee Provident Fund

Class 3

Digital Signature Certificate is the upgraded version of Class 2 Digital

Signature Certificate. By Using This Certificate You can

Participate/Bid in Any Kind of On-line Tenders/Auction across India. To

participate in the e-tendering process, every vendor is required to use a

Class 3 Digital Signatures Certificate.

- Applications of DSC

2. Income Tax

3. Foreign Trade

4. e-tendering/e-procurement

5. Employee Provident Fund

- What is an eToken?

USB e-Token can be

password protected so that Digital Signature is never lost when computer

is formatted or internet explorer changed. A virus cannot affect USB

Token, and the digital certificate stored would always be secure. As per

CCA's Office Order, with effective from 7th December, 2013, eMudhra

will be issuing Class 2 and 3 Digital Signature Certificates (DSC) only

on FIPS 140-2 level 2 certified crypto tokens. eMudhra recommends

TrustKey tokens. Trust Key token which is the most accepted, secure and

widely used token device in India for storing your Digital Signatures

- Difference between Encryption and Signing

Message encryption

provides confidentiality. Allows users to encrypt document with the

public key which can be decrypted only with the corresponding private

key. To put it in simple terms when encrypting, you use their public key

to write message and recipient uses their private key to read it. One

of the most secure way protecting confidential documents.

Message signing binds

the identity of the message source to this message. It ensures data

integrity, message authentication, and non-repudiation altogether. When

signing, you use your private key to write message's signature, and they

use your public key to check if it's really yours.

- Why eMudhra Digital Certificate?

eMudhra is a

Certifying Authority (CA) authorised by the Controller of Certifying

Authority (CCA) for issuance of Digital Signature Certificates in India.

eMudhra provides Class 1, Class 2 and Class 3 Digital Signature

Certificates (DSC) along with digital signatures for specific needs such

as Income Tax filing, MCA, e-tendering, e-procurement and Foreign

Trade.

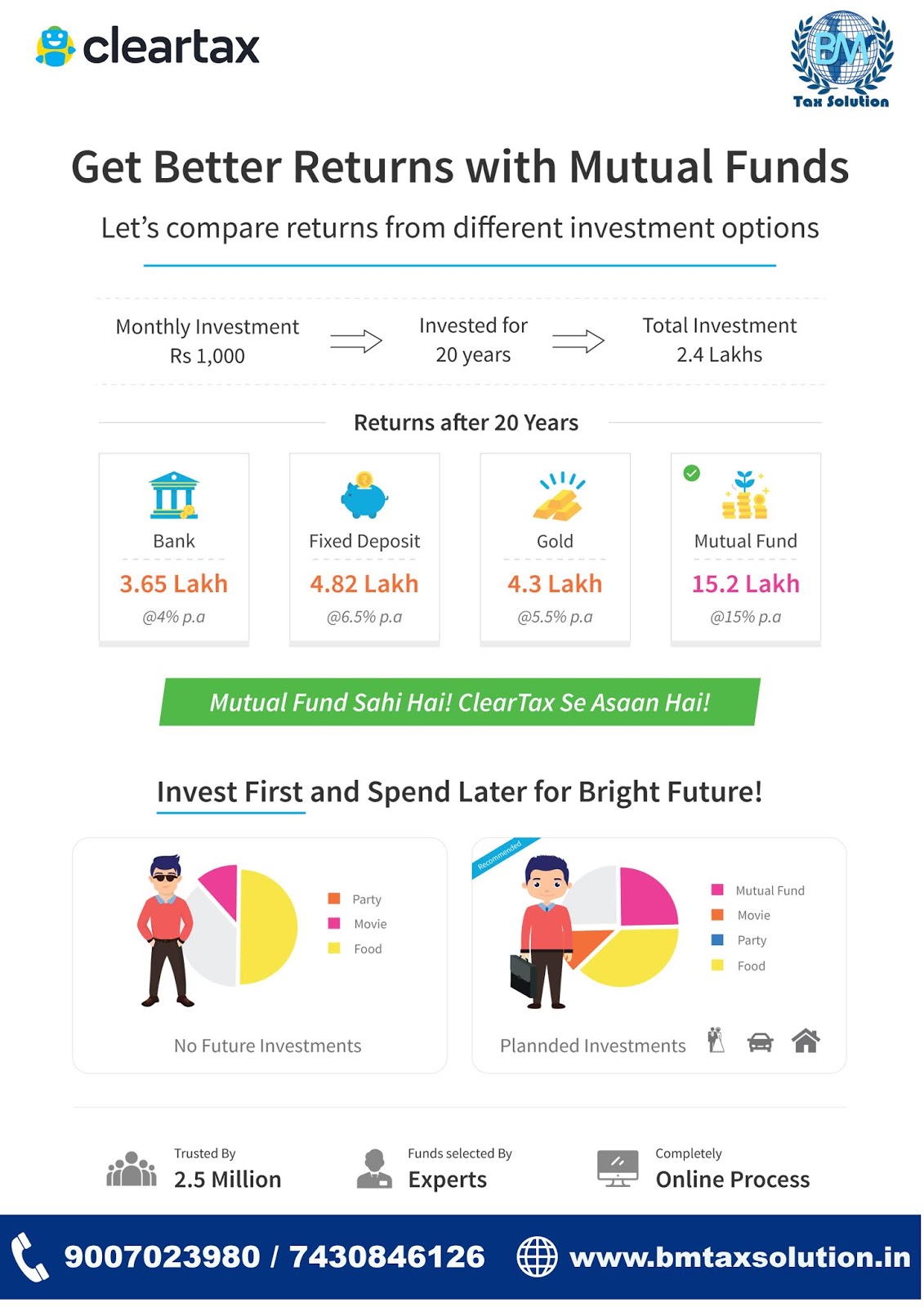

Invest in mutual funds starting as low as ₹500

Invest in mutual funds starting as low as ₹500